Accounting, End of Day and Year End

This section explains a number of common questions regarding accounting setup and daily or year end balancing

Event Settlement

Theatre Manager provides the supporting documentation in order to complete the settlement process. Often there are items negotiated that need to be calculated outside of Theatre Manager. An excel document should be created to calculate the final values in the settlement process.

REVENUE

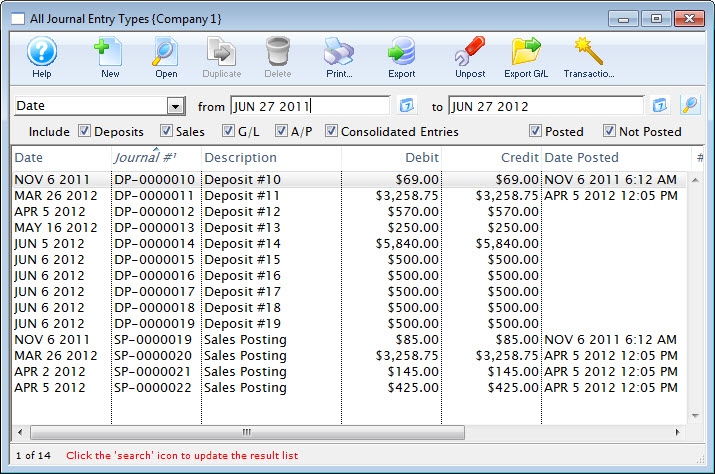

Theatre Manager will report the total revenue figure for the sales processed through the program.

| Step | Purpose |

| Step 1 | Run the End of Day Wizard.

Running the End of Day Wizard will post any outstanding sales transactions. It ensures all sales are journalized to the event. During the Sales Entries process ensure the option to Convert reservation-only orders to sales is set to Past performances only. Any tickets marked as Reservation Only for this past event will be converted to an Accounts Receivable. |

| Step 2 | Ensure the Event is in Balance.

Review the totals at the bottom of the GL tab within the event to make sure there are no differences. These totals can also be used to determine the total ticket revenue to be used in the settlement Excel sheet. |

| Step 3 | Clear up Event Receivables.

Run a Receivables-Based on Order Balances by Event report. The criteria would be Event # is one of (the event to be settled). This report will display any current receivables associated with the event to be settled. The value of the tickets listed in this report are included in all sales figures listed within Theatre Manager and any GL postings created during the End of Day. These receivables should be reviewed and managed before continuing with the settlement. If any changes are made repeat steps one and two above. |

EXPENSES

Before determining the total expenses for the event the contract should be reviewed. Often there are details in the contract that determine how certain expenses are to be calculated and who is resposible to pay them.

| Step | Purpose |

| Step 4 | Calculate Project Expenses.

If there is a Project for the Event within Theatre Manager review and finalize all tasks, resources and personnel. Changing the billing status for the Project to Invoice. Generate an Invoice and use the balance due to calculate the Project Expenses. |

| Step 5 | Outstanding Promoter Receivables.

This accounts for any tickets taken by the promoter to be sold at another location (consignment). The value of these tickets is included in the total sales reported by Theatre Manager however, the monies have not been collected by the box office. This amount should be deducted during the settlement process. To determine the quantity of tickets and amount to deduct a Tickets Sold/Revenue by Promotion & Price Code report can be generated. The criteria would be Event # is one of (the event to be settled). |

| Step 6 | Credit Card Processing Fees.

Run the Revenues by Payment Method-Ticket Based report. The criteria would be Event # is one of (the event to be settled). This report will list the totals collected for the event broken down by Payment Method. Since Theatre Manager allows for multiple payments on an order this report brakes out the values to the fourth decimal place to accommodate orders with more than one payment. Use the values in this report to determine the percentage or amount to be charged back to the promoter for processed cards. |

| Step 7 | Per Ticket Fees.

Often a per ticket fee is charged to the promoter for each ticket. If this fee has not been built into the ticket price and backed out of the Revenue listed above it should be calculated as an expense. If the fee applies to Complimentary or Consignment tickets it should be listed as a part of the settlement. Fees on free or promoter receivable tickets have not been collected. |

| Step 8 | Royalties.

If the royalties need to be paid by the organization and not the promoter these should be deducted as per the contract. To assist with the royalty figures a Revenue Summary for Royalty-Quick report can be generated. The criteria would be Event # is one of (the event to be settled). Royalties may apply to the copywrite or music used within the production. |

| Step 9 | Promoter Advances.

If any advances have been provided to the promoter these values should be deducted as a part of the expenses in the final settlement. Any amounts would have been negotiated outside of Theatre Manager and should be confirmed with the accounting department. |

Changing Tax Rates

In all cases of tax changes, consult your accountant for official rules

|

When a new tax rate becomes effective at midnight, it is very important you shut down the web listeners at midnight. Then not bring them back online until all the pricing changes and/or tax rate changes have been completed. This ensures all the web ticket sales after midnight are using the new tax rate. |

|

If you have not stopped your web listener please do not proceed. It is imperative the web sales be stopped at midnight the morning the tax rate changes. An end of day must be done and the steps below completed before online sales can be started again. |

Miscellaneous questions we've been asked:

- Do I need to create a new tax rate or can I just change the existing one? It's best to create a new tax rate. This will allow for more accurate reporting in the future and to keep better track of which tax rate was applied to each sale.

- Should I shut down the web listeners before midnight? You could, however, you may find there are many patrons attempting to purchase tickets at the last minute to avoid the new tax rate change. We recommend you keep the web listeners running as long as possible to allow for ticket sales as the pre-existing rate to make your patrons happy. However, the web listener should not run past midnight the morning the tax rate changes.

- Do I need to make all the changes to the pricing/tax rates after midnight or can they wait until the next day? Making the changes to the pricing/tax rates can be made the next day, as long as the web listeners and box office do not do any activity until the changes have been put into place and 'tested'.

- What happens when tickets sold at the old tax rate are exchanged? The rules and government interpretation indicate the 'old' tickets are refunded at the old tax rate and the 'new' tickets are subject to the tax rate in effect at the time of the exchange. Theatre Manager does this automatically for you.

- What should I do if there is a difference left over after "exchanging" tickets? When an exchange occurs it may be possible the patron originally paid more than the current value of the ticket. Depending on the organizations policy you may return this money to the patron, wave the difference, turn the balance into a donation or add an order fee for the value of the difference. If the difference in the exchange results in the patron owning you money then the next step would be to add a payment to the order and collect the required amount.

Steps that can be done in advance of the tax change

A. Rename the existing Tax Code to include the percentage value

|

If the tax code already indicates the percentage value move to step B. |

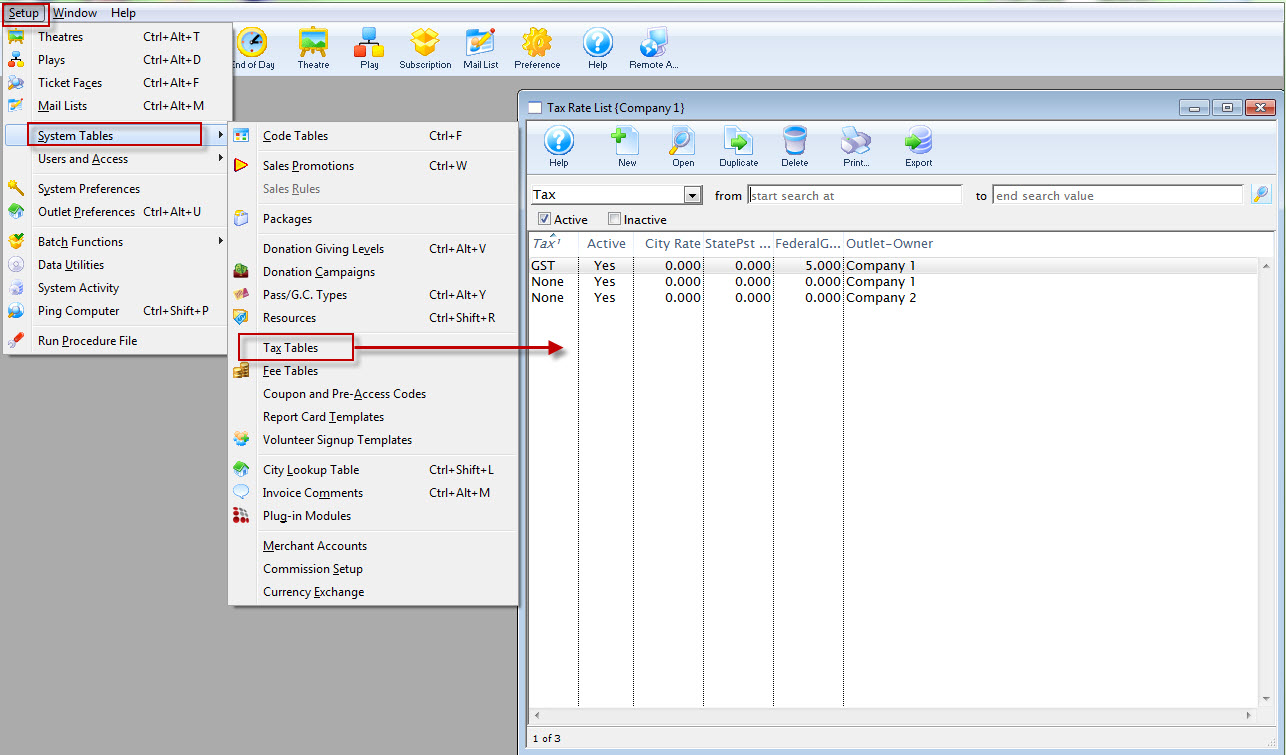

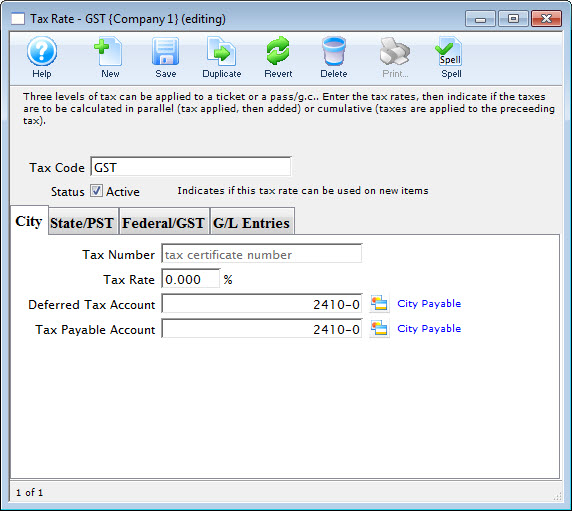

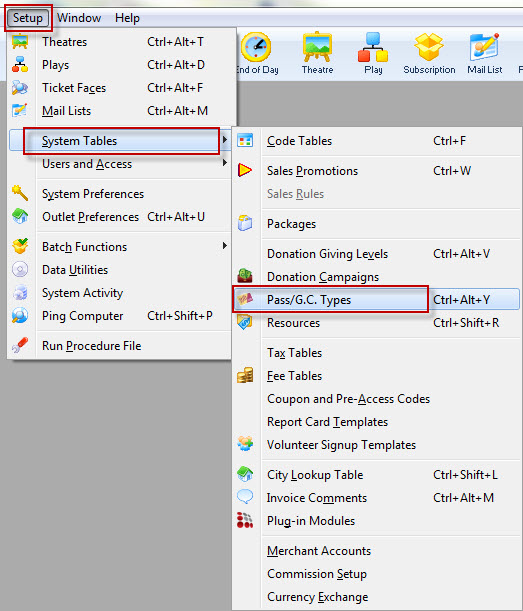

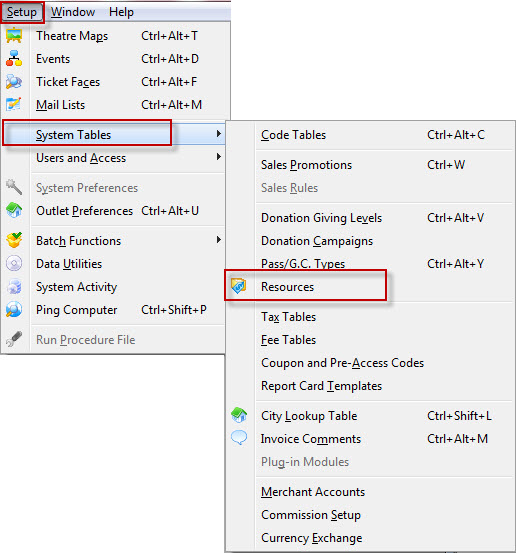

- Go to Setup >> System Tables >> Tax Tables.

- Double click on the old tax code currently being used.

- Change the Tax Code name field to something that included the percentage of the rate.

For Example:

Province Current Name New Name British Columbia Tax or HST HST 12% Ontario Tax or GST GST 5% - Click the Save button to save the changes.

B. Create a new Tax Code for the new Tax Rate

- Go to Setup >> System Tables >> Tax Tables.

- Click the

button to create a new tax code.

button to create a new tax code. - Set the name of the tax code to something to reflect the new rate.

Province Tax Rate British Columbia GST 5% Ontario HST 13% - Starting with the City tab, set the appropriate tax rate and G/L Accounts.

The G/L Accounts will likely be the same G/L Accounts that were used for the prior tax table.

- Repeat for the PST and GST tabs.

- Click the

button to save the changes.

button to save the changes.

Repeat steps A & B (above) for any other Tax Codes that contain the old tax rate. In a situation where the GL Account number is different click here to learn how to create a new account number.

|

For Step B above, you can change the name of the City tab in Tax Tables by going to Setup > System Preferences > Appearance tab and changing the right side of Federal Tax from City to HST. |

Steps to take when the tax change occurs

The following steps must be completed after midnight on the date the tax rates are to change and prior to sales beginning.

If you are running Theatre Manager's Web Sales module, make sure to shutdown all listeners by midnight. The Web Sales listeners can be restarted after the following changes have been made.

A. Make a Backup

The first step in making any major change to the database it to create a backup. A backup not only provides a starting point but it also means there is something to revert back to should things go wrong. For details on how to create a backup of the database click here.

B. Update Events

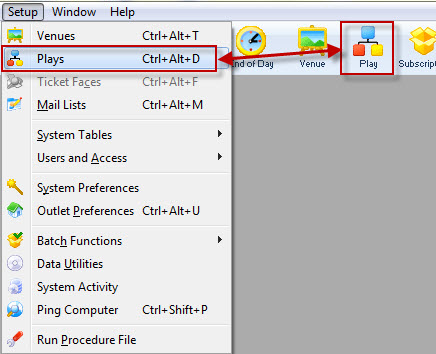

- Go to Setup >> Events.

- Search for an event that is currently on sale and double click to open it.

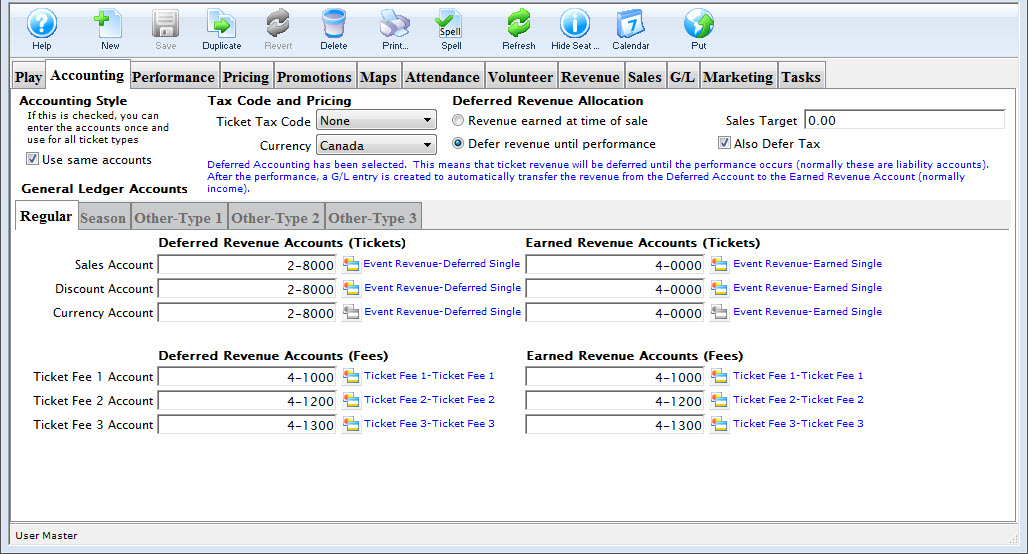

- Click the Accounting tab.

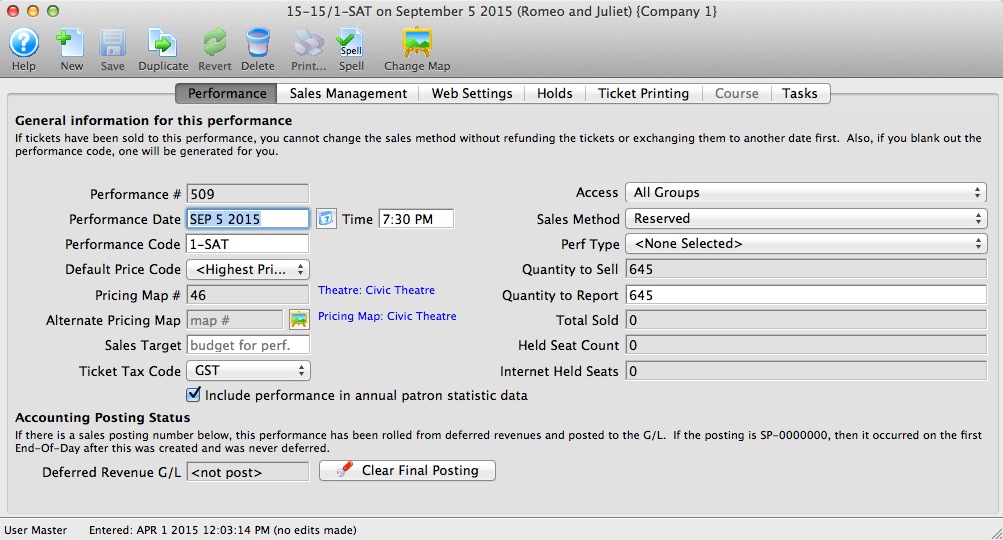

- Change the "Ticket Tax Code" from the old tax rate to the new tax table.

Changing the tax rate on the accounting tab changes it for all performances. If you wish to only change the tax code on a few of the performances, then do not change it on this tab.

- Double click on only those performances that are to be sold under the new tax rate.

- Change the Tax Rate Code in the Performance Detail window.

- Double click on only those performances that are to be sold under the new tax rate.

- Click the button in the toolbar / ribbon bar.

If tax is currently backed out of the ticket sales price, the value of the ticket will need to be altered under the Pricing tab for each Event. This is done by:

- Double clicking on the Price Code.

- Entering the base price of the ticket (including tax).

- Clicking the Calculate Price Excluding Taxes button.

- Repeat these steps for all other current and future events.

C. Update Ticket Sales Promotions

If the tax rate switch is instantaneous (i.e. it all happens on one day), then simple change the tax rate on the promotions.

However, if the tax rate is to be phased in, where an old tax rate applies to some events or performances and a new tax rate applies to other events and/or performances, you will need to create a second set of sales promotions to mirror the first and enable/disable them as appropriate.

For example, if a regular ticket can be sold with only Ontario Sales tax up till a deadline, but regular tickets for other events require HST, then you will need to rename your old 'Regular' to 'Regular RST' and add a 'Regular HST' promotion - and enable them as appropriate for performances. After the tax change is full implemented, you can merge the two sales promotions together if you wish.

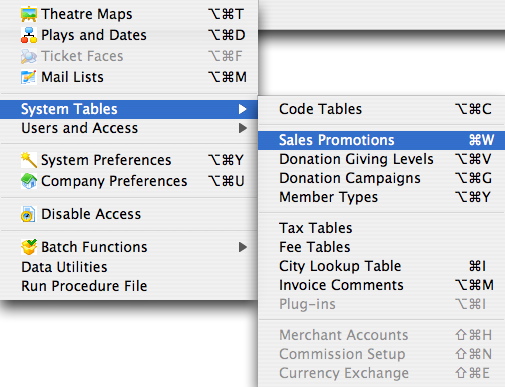

- Go to Setup >> System Tables >> Sales Promotions.

- Search for an active Sales Promotion

- Double click the Sales Promotion to open it.

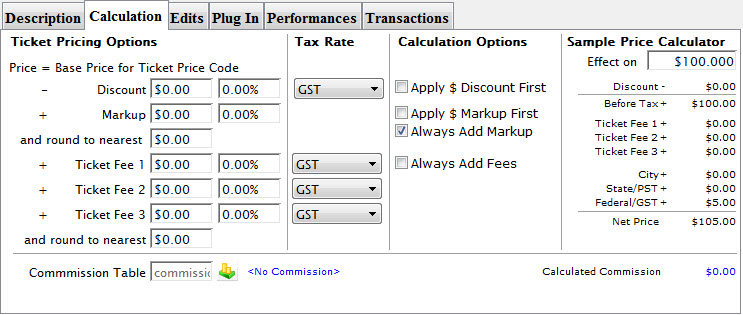

- Select the Calculation tab.

- Change the Tax Rate(s) from the old tax rate to the new tax rate.

There are four (4) tax rates per sales promotion that may or may not be effected.

- Click the button to save the changes.

- Repeat these steps for all other active Sales Promotions.

D. Update Memberships/Passes/Gift Certificates

In most cases, a gift certificate should not have any tax charged against it at time of sale as it is what called a 'financial instrument'. No taxes are payable buying a gift certificate and the tax is calculated at the time of exchanging the gift certificate for a ticket

Some items like a play pass or merchandise may have tax applied and could need to be changed. You will need to decide which passes/memberships or gift certificates are subject to the tax change.

- Go to Setup >> System Tables >> Member Types.

- Search for an active membership.

- Double click the membership to open it.

- Select the Accounting tab.

- Change the "Tax Rate" from the old tax rate to the new tax rate.

- Click the button to save the changes.

- Repeat these steps for all other active memberships, passes or items to be purchased.

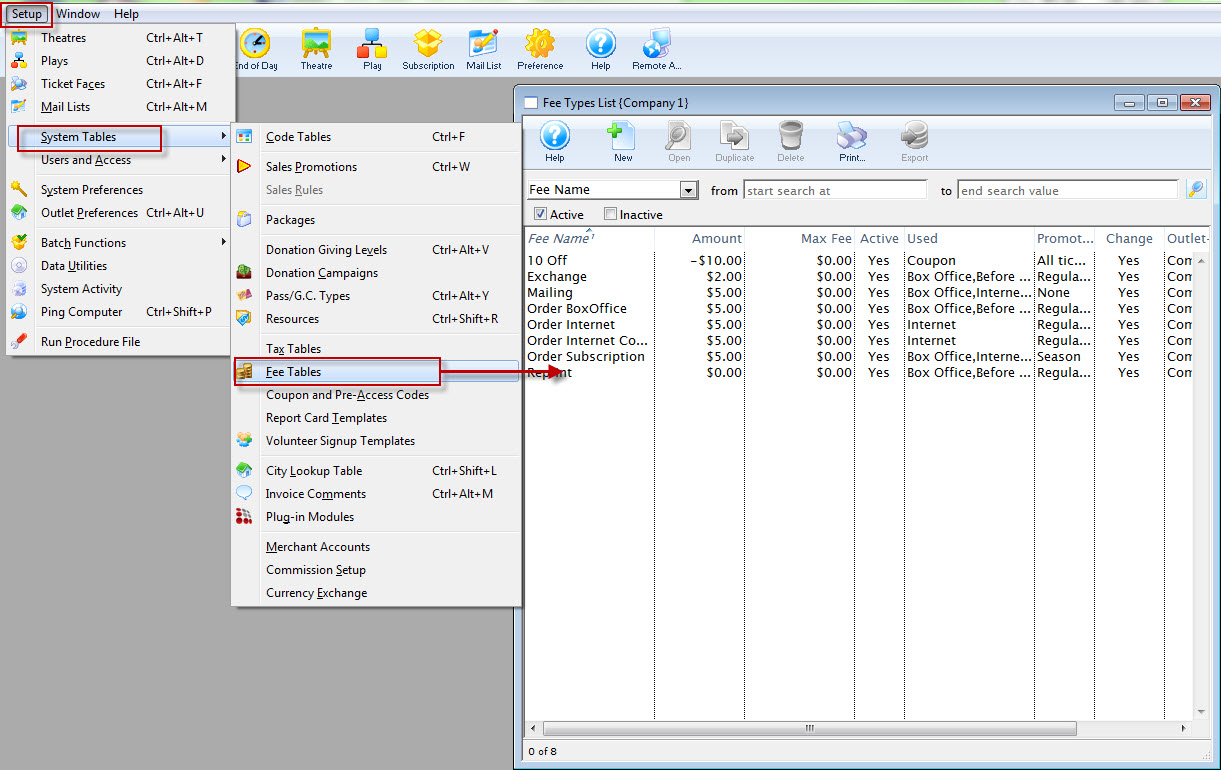

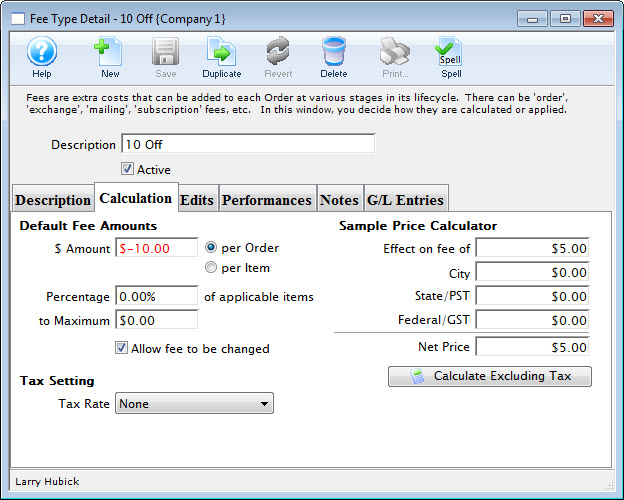

E. Update Transaction Fees

- Go to Setup >> System Tables >> Fee Tables.

- Double click on the first Fee in the list.

- Select the Calculation tab.

- Change the Tax Rate from the old tax rate to the new tax rate.

- Close the window to save the changes.

- Repeat these steps with all other Fees.

F. Update The Facility Management Module

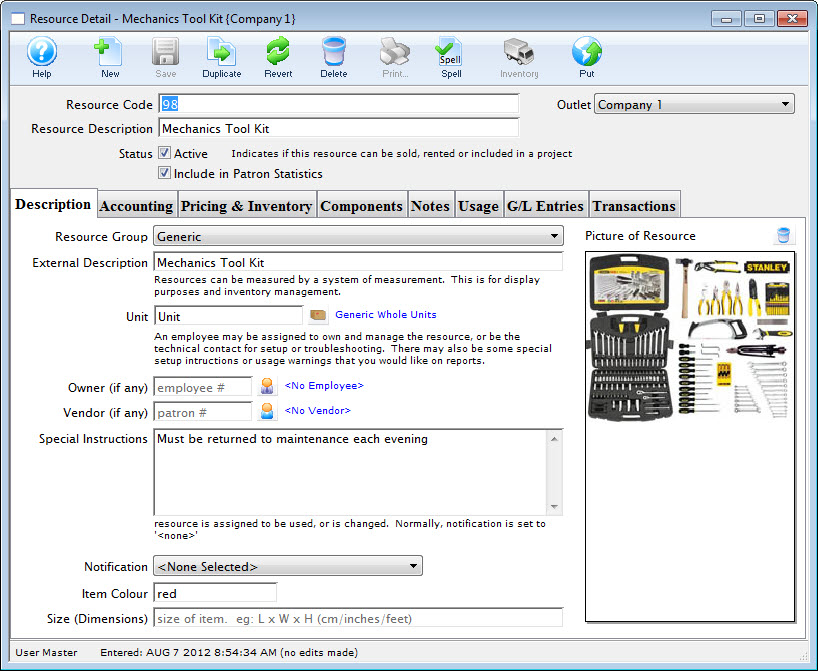

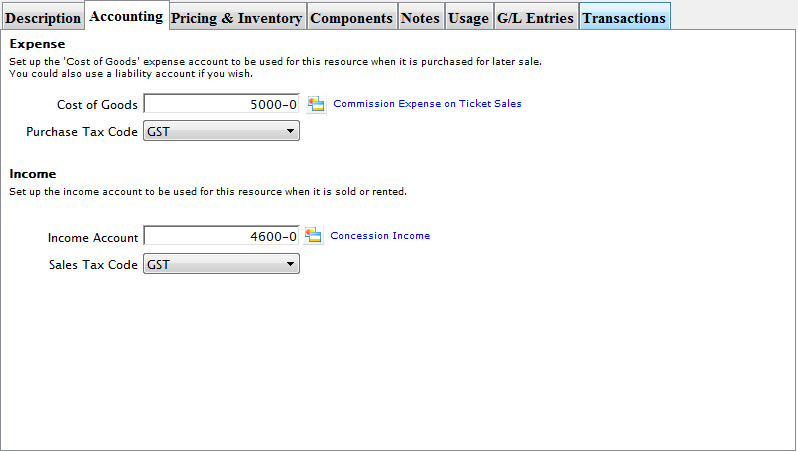

It may be necessary to update the tax rate on any projects where a future invoice is required. You may need to update resources and personnel for each task that spans over the date of the tax rate change for those projects that require billing.RESOURCES

- Go to Setup >> System Tables >> Resources.

- Double click on the first Resource.

- Select the Accounting tab.

- Change the Purchase Tax Rate and the Sales Tax Code from the old tax rate to the new tax rate.

- Close the window to save the changes.

- Repeat these steps with all other Resources.

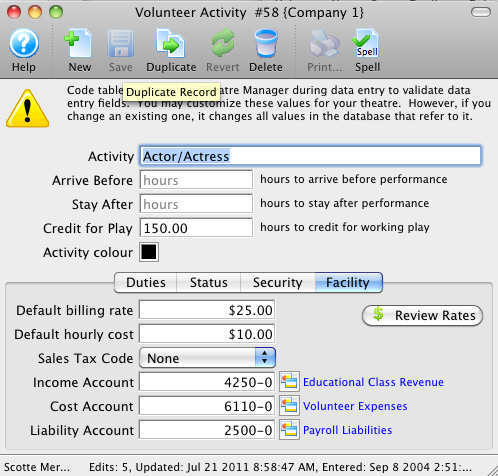

PERSONNEL/VOLUNTEER ACTIVITY- Go to Setup >> System Tables >> Code Table.

- Select the Volunteer Activity option in the left column.

- Double click on the first activity in the column on the left.

- Select the Facility tab.

- Change the Sales Tax Code from the old tax rate to the new tax rate.

- Close the window to save the changes.

- Repeat these steps with all other Resources.

Congratulations! New sales may now be processed, and all Web Sales listeners can be started.

Transitional rules: HST on Ticket Exchanges bought before HST implementation

The Arts Management team are not tax accountants or experts, so Theatre Manager is designed to implement a somewhat safe interpretation of the rules. These rules were generally acceptable for the Maritime provinces HST transition some years back.

Please read the examples below that are taken from Ontario Transitional Rules and do check with your accountants. There is enough in this document to warrant taking the safer road on the taxation side. As I said, we are not tax accountants, so the actual rules may be different, or there may be specific exceptions that we are not aware of.

The approach that you can take in TM to handle exchanges is:

- new tickets (and exchanged tickets) get the new tax rate that applies to the performance

- refunded tickets are refunded at the tax rate used to buy them

- venues who want to implement what are effectively tax rebates on subscription ticket exchanges need to discount the final order difference using a negative order fee to write off the HST. It will come through the end of day as 'negative' tax, but in the end, that is good because you can track it as an input tax credit.

This assumes that it is legally valid to do that. Please please please, talk to your Accountant for your specific situation.

Background History to the TM Transitional Rules

The rules that we've been observing are are found in a published web article by the Ontario Government.

| There is a small section in this document near the bottom labelled Returns and exchanges near example 28 which is excerpted below. it is the subsequent caveat that is the most interesting.

Example 28: In July 2010, a person returns a shirt that was purchased in June 2010 for $40. The vendor exchanges the returned shirt for another shirt that costs $60. In this situation, the vendor would collect the Ontario component of the HST on $20.

If the RST did not apply to property that was purchased before July 1, 2010, and it is exchanged on or after July 1, 2010, the Ontario component of the HST would apply to the full consideration for the replacement property.

Tickets generally have no RST. By that interpretation, exchanges for events that occur after July 1,2010 would be charged the HST on the full amount, even if bought before May 1, 2010. |

|

Example 22 speaks to tickets (albeit a circus example) and has an implication that shows across the boundary of july, but sold earlier than May (i.e. buy now, go later), should probably have HST in them in the first place. It states:

Consideration due or paid on or before October 14, 2009: Notwithstanding the general RST wind-down rules, the RSTA would apply where consideration for a sale of goods, services or admissions becomes due or is paid on or before October 14, 2009.

Example 22: In September 2009, a vendor sells tickets to a circus show to be held in July 2010. The RST would apply to the price of admission.

Interesting interpretation of this is that if you were not charging RST (because you were exempt), then you cannot use the 'difference on the exchange' from example 28. Otherwise, you might be able to take advantage of example 28 - but you would have to have been charging RST on tickets last October. |

|

Revenue Canada speaks to a transitional rule with a ticket example using Stratford Festival. It has a specific example where tickets are purchased after May and the performance is in July. It clearly states that HST applies. Revenue Canada speaks of a transitional rule that follows:

The HST will generally apply to a service to the extent that the service is performed on or after July 1, 2010. The HST will generally not apply, however, to a supply of a service if all or substantially all (90 per cent or more) of the service is performed before July 20 Our reading of that suggests that a subscription where 10% or more of the ticket value is after July 1st suggests that HST should be applied to the initial sale. |

| There are some exceptions to the transition rules listed in various places.

We took a representative example from Tax Tips for subscriptions. In every interpretation we've seen, this means magazine periodicals. Anything mentioning tickets refers to transportation. Nothing specifically talks to non-profit arts organizations exchanging subscription tickets when a new tax rate applies. |

|

Finally, there is a small note in the Ontario Transitional Rules document called 'anti-avoidance'.

It looks innocuous - but the meaning is clear - if the Government thinks you are doing something to avoid the tax (they coin it 'blatant tax avoidance arrangements', then trouble looms and the department of finance can make any rule they want. So, 'buy your pass now to avoid HST next year' may (or may not) be on that 'tax avoidance arrangement' category. Anti-avoidance Existing anti-avoidance rules in the ETA (Excise Tax Act) would apply to transactions to which the general transitional rules for the HST apply. Additional anti-avoidance rules may be implemented in order to maintain the integrity of the GST/HST and the RST during the period of transition to the HST in Ontario. The legal ruling from University of Toronto is provided for your reference. Would the Government prosecute? Might not, it may be bad press. On the other hand, Governments like their tax revenue, so they might, especially if it amounted to a significant tax influx when you consider the value of all advance subscription tickets sold for all venues in the entire Province for a year. |

I hope these references help. If you are confused, I can understand it. Our reading is not necessarily correct, but in the absence of a very specific printed ruling, we've chosen to play safe, yet give the venues an option of using a negative order fees to effectively claim back the tax if that is what they wish to do.

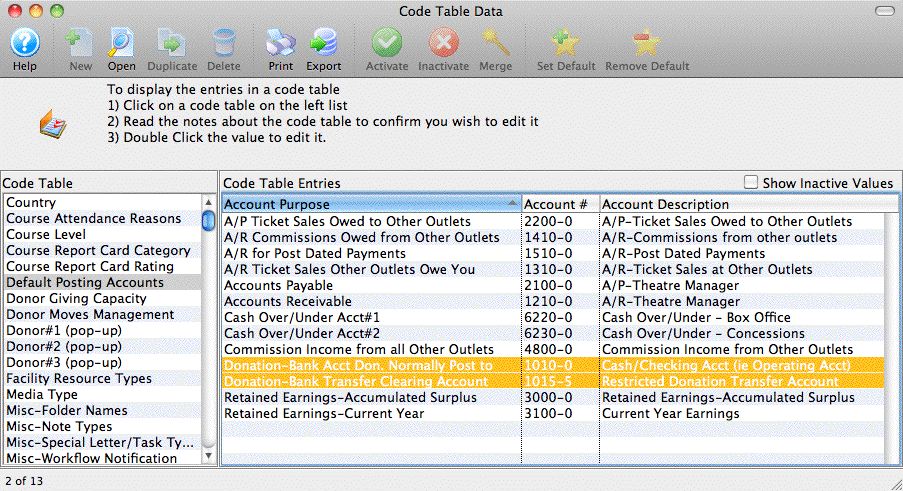

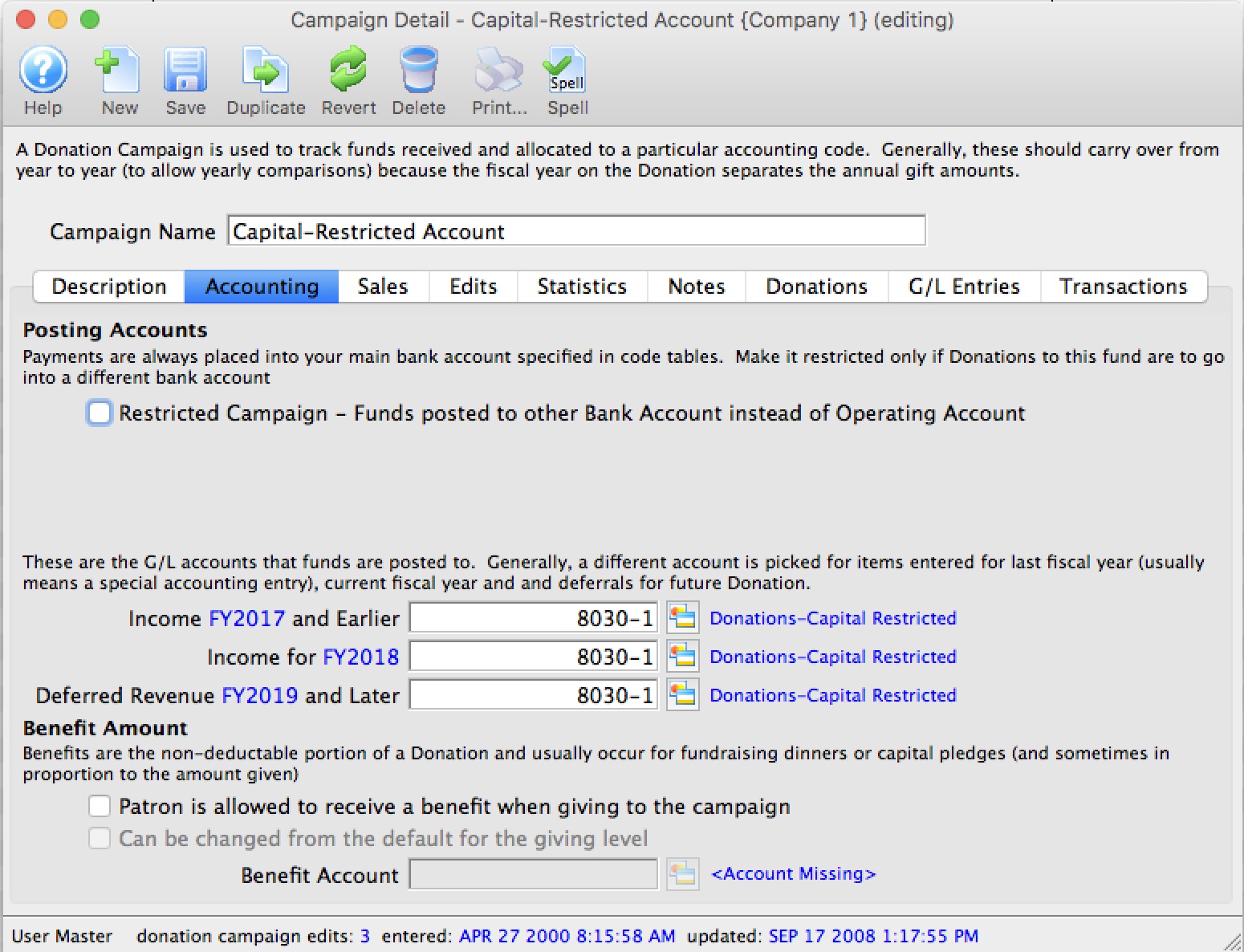

Donation Clearing Account

- the Donation Account Donations Normally Post to -and-

- the Donation Bank Clearing Account

To set this up, you would change the BANK ACCOUNT in the Campaign setup to the restricted GL account you have assigned to the separate bank account.

In this example, let's assume your general CASH GL account is 1000, and the Capital Campaign GL account is 1008.

|

While the payments for all sales goes into the general operating account at the bank, and the majority of your campaigns are sending those funds directly to the standard 1000 GL account, the Capital Campaign is going into the 1008 account. |

GL entries for the restricted Donation - no payment yet

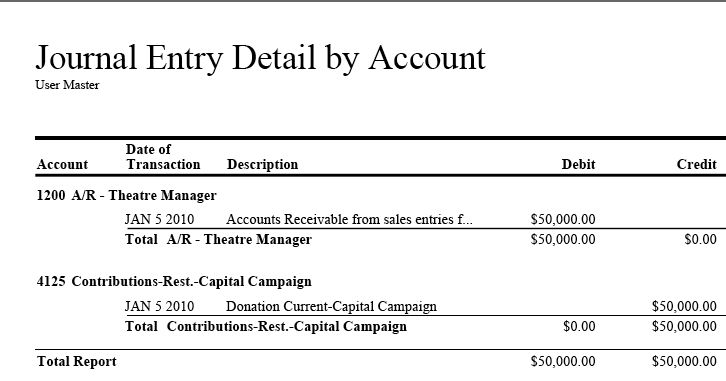

The next assumption is that a $50,000 donation is pledged - but not paid - to the capital campaign. This simply increases A/R by $50,000, and increases the Capital Campaign donation GL account (in this example, 4125).

GL entries when part or all of the payment is received

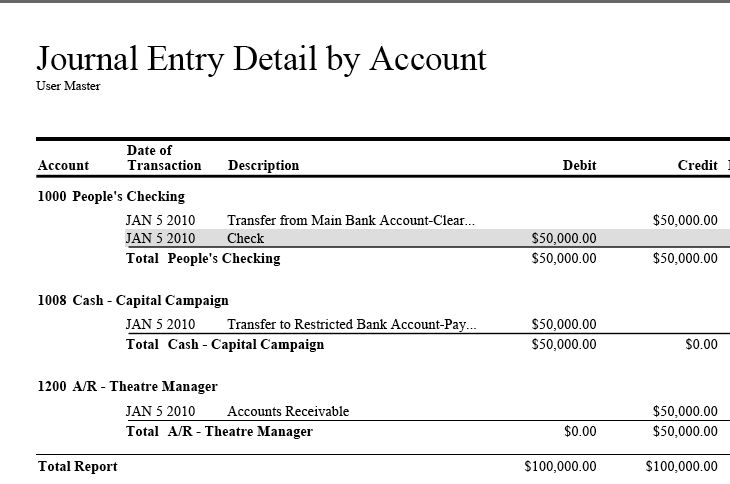

When the donation is paid (either in part or in full), Theatre Manager will tell you through the End Of Day reporting to move the funds from where they were originally posted to the separate bank account.

What this means to Finance

To understand this report, first remove the simple offsetting transactions for Accounts Receivable. eg:

- The final transaction reduces the A/R - and-

- and the second transaction increases the CASH account by $50,000, which is the amount of the payment.

- These are the same transactions we see for every payment in Theatre Manager. Reduce A/R, increase cash.

That leaves us with the two transfer GL entries.

- The first is the Transfer from (1000).

- It is a credit for $50,000

- meaning that you are going to need to manually take the funds OUT of the cash account (main bank account) using your online banking

- The second is the Transfer To:

- which moves the money IN to the other bank account

- which is 1008 (because that is where you are keeping the actual money for the capital campaign).

|

The Only action you need to do is watch for the transfer out and then do something outside TM to move the funds from your operating account to the restricted asset account for the campaign when the payment is made. |

Donation Clearing Example Setup

Code Table Default Accounts

The two highlighted accounts below are what makes the automatic creation of G/L entries for transferring donations to the restricted account work.

- The first is the Donation-Bank Acct. Don. Normally Post To. which really should be the same account number as the operating account. When you look at a normal donation (second picture), you will see this account is placed into the 'Bank Account' field

- The second is the Donation-Bank Transfer Clearing Account. This will be an asset clearing account - which in general means that if something gets posted to this account, you will need to make a manual GL entry in your accounting system to get it moved from this holding place to the right bank account

Typical Donation - Non Restricted

This sample shows how the bank account is entered for almost every donation campaign. Typically these would be referred to as non-restricted. Theatre Manager will put any payments received against these donations into the operating account

Special Donation - Restricted

This sample shows how the bank account is entered for a donation that is deemed to be 'restricted' - meaning the money needs to be moved to a different bank account, or accounted for in some different manner. When the donation is paid for, Theatre Manager will create a clearing entry for you to this account.

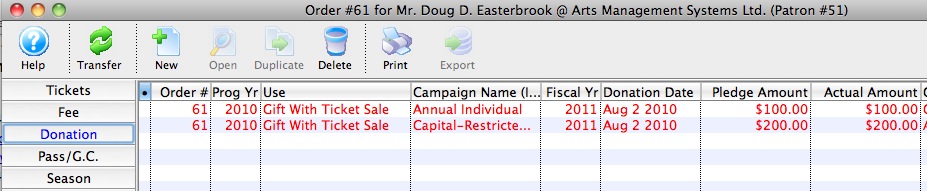

Example of an order

This picture shows an order with two donations in it, one for each of the donation campaigns described above.

Sales Posting

When the sales posting is created, you can see that each of the donations is placed into its own sales/income account. This will happen whether or not there is a payment yet.

Deposit Posting

When the payment is received at some time after the donation is entered (it could be right away, or the payments for some donations can be received in installments), running the deposit process is intelligent enough to:

- Put the entire check into the cash account

- Decrease the receivables account like any other payment

- Add two special entries that offset each other

- The first entry from Theatre Manager is telling you to put some money into the restricted bank account because a payment was received for the donation

- The second entry is in the restricted donation transfer account. Normally the total value of funds in this account is zero. However, as payments for restricted donations are received, this account will increase in size. Theatre Manager tells you which donation the funds are for. At some periodic basis (daily, weekly, monthly), you will need to clear this account to zero. To do this, you go to your web banking and transfer funds from your operating account over to the various restricted accounts as identified by the clearing account.

End Of Day Settlement over an Extended Break

|

The easiest way to handle an extended break (eg over the christmas holidays) where there are no events being performed and nobody is in the office is to temporarily enable the Emergency Mode on the merchant account.

This is probably the best option if nobody is around |

|

Alternately, you can let cards be authorized, but you will need to check with your credit card processor to find the maximum period in which credit cards must be settled before they are automatically released.

If you can remote in and periodically do a deposit, this is probably the best option |

Options for processing over an extended break

On an extended break, and if you have web sales occurring, deposits still need to take place on a regular basis. Therefore, your options are to do one or more of the following:

- Turn your merchant processor into Emergency Mode over the holidays when nobody is in the office. This option is probably the easiest and means:

- All credit cards taken online will the treated as post dated payments (they can be authorized for real when you get back)

- You might be taking a small risk that the card get declined, but since no tickets have gone out and (assuming that there are no events performed during this time), you have complete control of your inventory, including refunding it if need be

- When everybody returns from break, turn off Emergency Mode and authorize all cards at end of day

- Stop all sales during the break, including Box Office, Web Sales and any donation entry by the Development Department - essentially 'close the shop'

- Come in to the office and do your deposits every few days

- Remote into your company network from your home office and perform your deposit.

- Do a final deposit before you leave the office and then one first thing when you come back (read the cautionary note)

Caveat for Options that do not use the Emergency Mode Feature

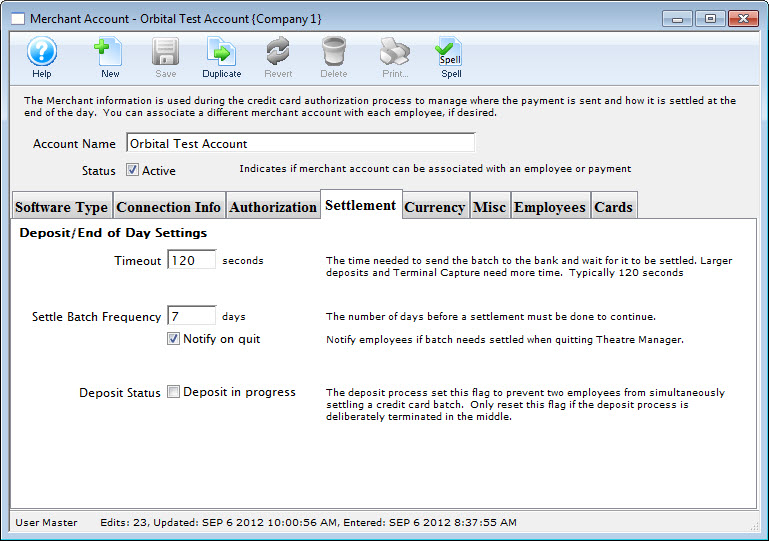

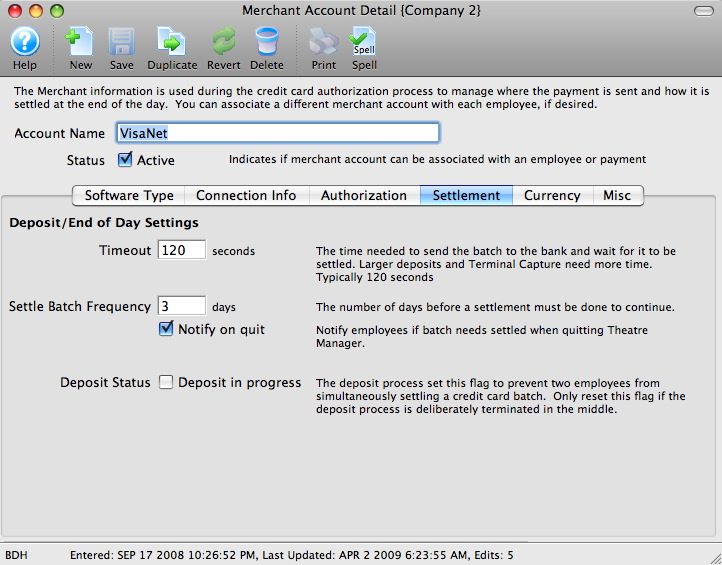

Your credit card processor (Chase Paymentech, Authorize.net, Elavon, Moneris, etc.) prefers that you settle your credit card batch on a regular basis (i.e. daily). Your merchant provider sets a specified maximum frequency between settlements so that they can guarantee that the amounts they have authorized for you will still be available when you go to collect the funds. Because authorized credit cards must be settled within the pre-defined frequency, there is a "Settle Batch Frequency" setting in the Setup>>Merchant Accounts>>Settlement tab that retains the maximum days that your merchant provider indicates before a settlement is required. The maximum setting in Theatre Manager is set for seven days before settlement is required, however it is recommended that this is set at three days in order to maintain clean batches and regular settlements.

This setting applies to Box Office Sales only, and if you are running web sales over an extended break (such as the end of year holiday season), your web sales will continue to authorize credit cards beyond the time out setting in Theatre Manager.

|

For most online payment gateways (Paymentech Orbital, Authorize.net, etc.) the actual timeout may be up to 30 days or longer and having a extended break of less then 30 days may not have any impact on your non-settled authorized cards. Check with your credit card processor to determine the maximum period in which credit cards must be settled. Some credit card processors offer the service of auto-closing your batch if you plan to be away for an extended period. If you choose this option, you will need to force your deposit when you return from the break, after ensuring that Theatre Manager and your processor have the same credit cards and amounts in your batch(es). Check directly with your processor (Chase Paymentech, Authoriza.net, Elavon, Moneris, et.c) to see if they offer this service. |

|

You do not need to perform a complete End Of Day (Deposits, Sales Entries, A/R Posting, and Reports). You only need to complete the Deposit portion of the End Of Day in order to settle the batch. |

Option 2:

Turning off web sales means you do not need to come in at all. If this is a time of year when you do not have many online ticket sales, gift certificates, passes or donations, this may be an acceptable option for you. Unless you have a need for this approach, it is really not recommended.

Option 3:

If you can stop by the office once every few days (within the limits of the Batch Settlement Frequency), then you can run the Deposits in order to clear the open batch. You do not need to run the full End Of Day until you return from the break if you do not want to. This is a reasonable solution.

Option 4:

The more likely option is to remote in to your company network from your home office and perform the deposits. You can (along with your IT department's permission and direction) use a remote connection to access your company network and run the End Of Day from your home. If you are running web sales only (and have an online payment gateway), you may choose to delay the End Of Day until you return to the office, as long as it does not exceed the time specified by your processor. This is probably the best solution

|

If you choose to use remote access to log in from your home office and complete the deposits, check with your IT department to ensure that you abide by the security rules and protocols they have defined for your company network. |

Option 5:

This is the default or do nothing alternative but you will have to verify with your credit card provider how long you can go without settling your batch. Most credit card providers are quite liberal and allow a relatively long time of a week or more which means you should not have any issues.

|

There is one service provider we know of (Global Payments - NDC) that starts dropping any authorizations that are older than 3 days as if they never happened. Since they don't tell you, this is a huge problem and you will need to pick one of the other options.. It is one of the reasons we recommend against using them as a service provider. |

Remote Access Options

At Arts Management Systems, we use TeamViewer for its ease of use, and the fact that in most cases it does not require a firewall configuration. There are several other remote access programs available, including:

- Remote Desktop Connection

- Apple Remote Desktop

- PC Anywhere

- LogMeIn

- VNC

- Timbuktu

|

While Arts Management Systems does not directly support any of the above products, we have tested each one and know they work for remote access. Installation, licensing requirements, and operation of any remote access product is the client's responsibility. |

End of Day Settlement Warning

For example, Global Payments is notoriously strict and starts removing credit card authorizations that have not been deposited within 5 days - which throws out the settlement balance (one reason we recommend not using them as credit card processors)

You can alter the 'batch settlement frequency' which is the number of days before the End of Day Settlement Warning appears'.

|

Arts Management Systems strongly recommends contacting your Merchant Provider to find out what their policies are before altering the default. The number of days the batch can remain open depends entirely on your account setup with your merchant provider. |

- Click Setup >> System Tables >> Merchant Accounts.

- Double click on your Merchant Account to open it.

- Select the Settlement tab.

- Alter the Settle Batch Frequency field as desired.

- Click the Save button at the top of the window.

- Close the Merchant Account Detail window.

|

You may be prompted to enter contact information for your Merchant Provider prior to closing the Merchant Account Detail window. Please ensure you have a Contact Name, Phone Number and E-mail Address for your Merchant Provider ready. This is used to tell employees whom to contact if there are issues with the credit card and the phone number to call at the credit card merchant services support line. |

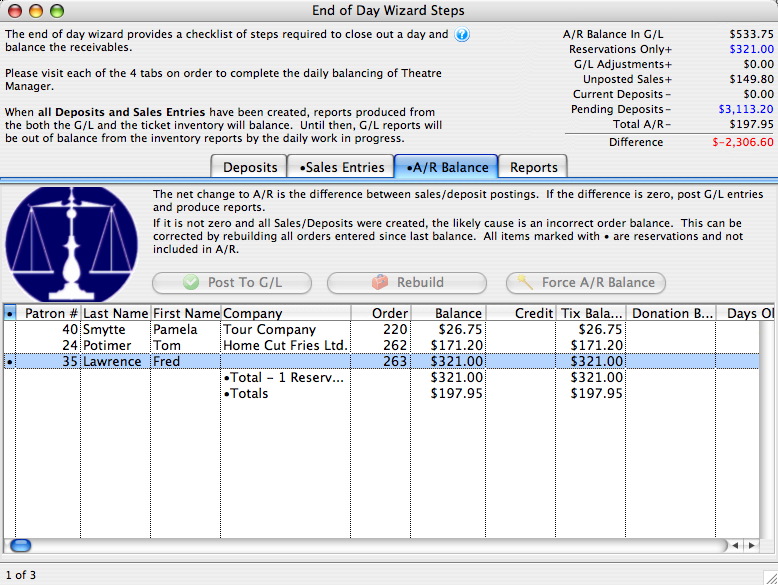

How do I correct an End of Day Imbalance?

If you are running into problems trying to bring the daily imbalance to zero in end-of-day, then please follow the troubleshooting steps at fixing an imbalance

How do I tell which payment method paid for a ticket and why can it only be inferred from a payment allocation report?

|

We are often asked how to find out how many tickets were paid for using various payment methods (for example: Visa, Master Card, cash, etc.). There is definitely a need to do so for many reasons:

|

There is a method to find a very very close (but approximate) answer for business purposes. You cannot find an exact answer of '1 ticket paid for by visa' for the reason illustrated in the example below. If you are trying to manage your receivables, please refer to this web page that describes the use of Accrual Accounting in Theatre Manager.

Getting a reasonable approximation

The reasonable answer can be obtained using the Revenues by Payment Method-Ticket Based report or looking at one of the royalty reports. The process for these reports are to:

- Run the 'Receivables-Based on Order Balances by Event' to see if anybody owes you money for the event. If there are any receivables, clear them out or pay them off.

- Find all the orders for the tickets you need the answer for - e.g. you want the calculation for all tickets sold at a particular show, at the end of the run, to obtain credit card discounts paid - and which can be deducted from royalty payments.

- Theatre Manager then finds all the payment methods for the orders and allocates the payment method among the tickets in the order.

- The allocation is then printed on the report. Please refer to the examples below to see how this can work.

Why can't the number be exact?

|

We will use an example of why the question being asked is not available in ANY accounting system. That is - specifically what payment method paid for an item out of inventory cannot be accomplished in accounting system. It can be inferred, but there is no way of ascertaining 'fact'. |

First, Theatre Manager uses accrual accounting. This means each payment decreases accounts receivable. Each purchase increases accounts receivable. In a perfect world of buy one ticket for $10 and pay $10 in cash, it can be inferred that 1 ticket was paid for with cash.

What if the transaction gets complicated?

Now we will use a real world example. A patron purchases a play pass for $100 and donates $50 at the same time. He is sharing the pass with a friend. You receive $50 from the friend by visa (the friend donated separately earlier in the year) and the patron pays $100 with Mastercard. Question: How many tickets were paid for using visa? Answer: It can be inferred:

- None because it is a play pass and they have not yet been used.

- In fact, if they are never used, the answer will be zero.

- A possible answer is 50/150 = 33% of the pass - as that is the exact ratio of payments made on this order and you don't know the patrons intent.

- A possible answer is 50/100, if you knew the patron's intent.

So far, there are 4 possible answers for the transactions. All, are in fact wrong. The simple answer is that when the pass was purchased, it increased receivables because something was sold from inventory and the payment decreased the receivable.

Time passes and the patrons use the pass to buy tickets. At this time, the payment method for the ticket is part of the pass and we are now a few steps removed from the original transaction. If the patron allows other patrons to use the pass things are further complicated.Finally, the patron may decide they can't use all the pass, so they turn it in for a donation receipt or you write it off to un-earned revenue.

These kinds of transactions happen with amazing regularity at any theatre company.

How do other industries do this?

They do not. If you pick any another industry - such as a lumber store where you buy some lumber, some screws, a new power tool and pay with a gift certificate you got for christmas and top it up with some cash in your pocket and then use a debit card, you could be asking the same question.

Did my gift certificate pay for my cool power tool, or did it pay for my screws? again, the answer is: YOU CANNOT PROVIDE AN EXACT ANSWER OF WHAT PAID FOR EACH INDIVIDUAL PIECE OF INVENTORY (only an approximation).

Summary

- In an inventory management system, it is never possible to clearly determine how each item is paid for that was removed from inventory.

- There is no accounting system that we know of that provides this capability in any of its reports.

- Theatre Manager recognizes that there is an advantage to being able to approximate the answer with a degree of precision and provides report to allocate payments to tickets at the end of a run for purposes of royalty deductions. These are accurate to 4 decimal places and fractions of tickets.

If you require further clarity on this concept, please consult with your accountant or auditor.

Managing or cleaning up your receivables

- there are multiple orders for same patron with offsetting balances (eg total debits minus total credits = zero), so the patron does not owe you anything

- the order is so old as to be uncollectible - and you need to write off the balance

- there is a small balance in the order (generally a fee charged or waived) that puts the order out of balance and just needs fixed without bothering the patron

- this is a true receivable - and the patron still owes you for product

- this is a true over charge and you should be refunding money to the patron or converting it to a donation

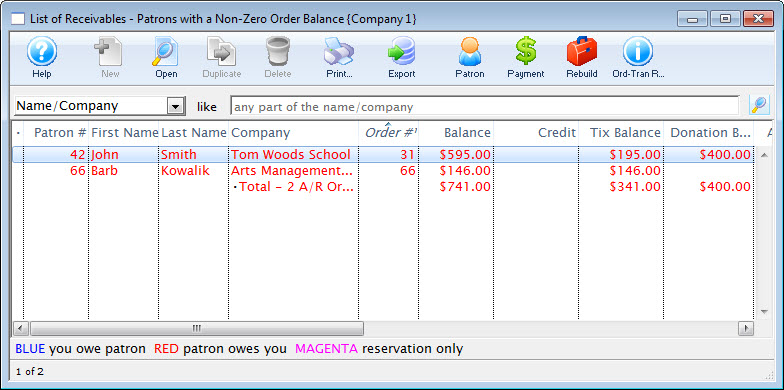

Identifying Receivables

All you need to do is:

- Look at the receivables listing using Accounting->Receivables->Receivables Listing -or-

- Look at the same data in the A/R Balance Tab in the end of day process, if that is more convenient.

- View the data on the Receviables - Based on Order Balances report which can be printed from the reports button under the Orders and Payments category , the Reports Tab on end of day, or right clicking on either of the two windows above and printing the A/R report.

Same patron with multiple offsetting orders

Offsetting orders are where the patron owes you money for an order and you owe them money for another order. This often occurs where the box office staff refunded the tickets (but not the payment) and then bought more tickets on a separate order instead of adding tickets to an existing order. In general, the patrons owes you $xx.xx and you owe them $xx.xx. Cleaning up these orders and removing them from the receivables list is as simple as:

- highlighting the appropriate orders from the list belonging to the same patron # -and-

- Applying one payment to multiple orders - using the cash payment method.

Orders that are so old as to be uncollectible

During followup training, we often see some orders that have been around for a decade or more with an unpaid balance. Unless it really is a long term receivable for a major donation, it should be written it off so that it does not clutter up the receivables listing. A messy receivables listing may lead you to ignore a true balance owing.

The steps to do this are:

- If you do not already have a payment method for write-off or uncollectible debt, you will need to make one in the Payment Methods code table. Once you have a write-off payment method set up with the correct account approved by finance -then-

- Select the order with the uncollectible amount (on any list that shows orders)

- Right click on the order from the list

- select Apply a payment to open the payment window

- use the write off payment method

Orders with a small balance

Order with a small balance generally have a recognizable amount in the order balance. For example, it might be $3.00 and that could represent an order or mailing fee that should have been charged -- or was possibly waived. If that is the case, then it is suggested to alter the order and fix the missing data by adding or removing the fee.

Use this approach when you want to ensure the correct money goes through to the appropriate order fee G/L.

To do this.

- Double click on the order.

- click on the fee button

- add or remove the fee to bring the order into balance

- Close the order window

This is a true receivable

Do nothing to the order - leave it as is.

Unless, it s for a receivable way in the future such as a group ticket sale or donation for months in the future. It is a good idea to set the expected payment date in the Contractual Notes tab in the payment.

Setting the order as a future receivable helps as it changes the age of the receivable so that it is always current, until the future date arrives. In effect, you are telling TM that you don't want to bother with this receivable for a while - and it clearly identifies it.

This is a true overcharge and you should be refunding money

If the balance indicates that you owe the patron money (and its large enough), there are three suggestions.

- If the patron wants to carry a balance, you could convert the balance to a dollar value gift certificate which you could call Store Credit. This could allow them to redeem their credit online (if it is set up that way).

- Double click on the order to open it

- Click on the gift certificate button

- Add a gift certificate to the order

- If the balance is larger, you could approach the patron and turn it into a donation

- Double click on the order to open it

- Click on the donation button

- Add a donation to the order

- You could leave the balance as is or add something to it like a fee as per above

- of, if you do need to refund the money, you can create a refund payment

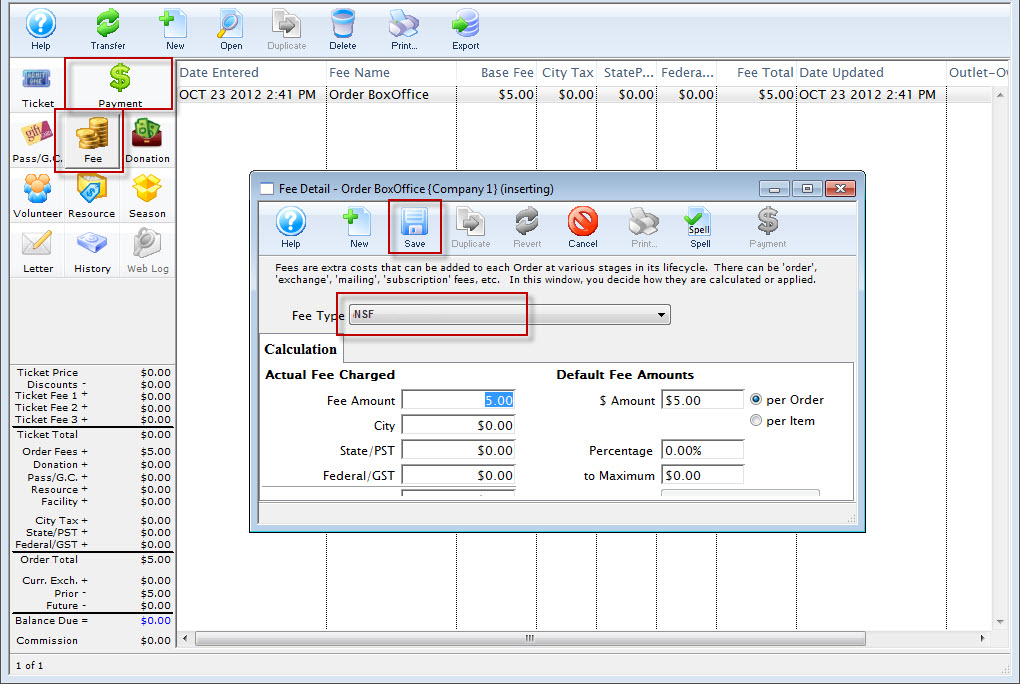

NSF Cheques

Tracking NSF information is a good idea. When you put the information in Theatre Manager it will tell your accounting department what needs to be done. It will also allow for you to have a record within Theatre Manager of this patrons payment history which may be used in the future to determine if you allow this patron to continue to pay by cheque.

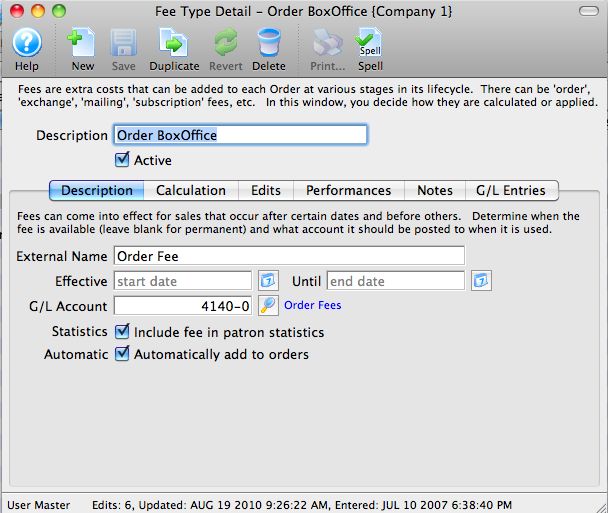

Some organizations charge a fee to the patron for NSF payments. This is done by setting up a new fee option in Setup >> System Tables >> Fee Tables. Click here for the steps to set up a new fee.

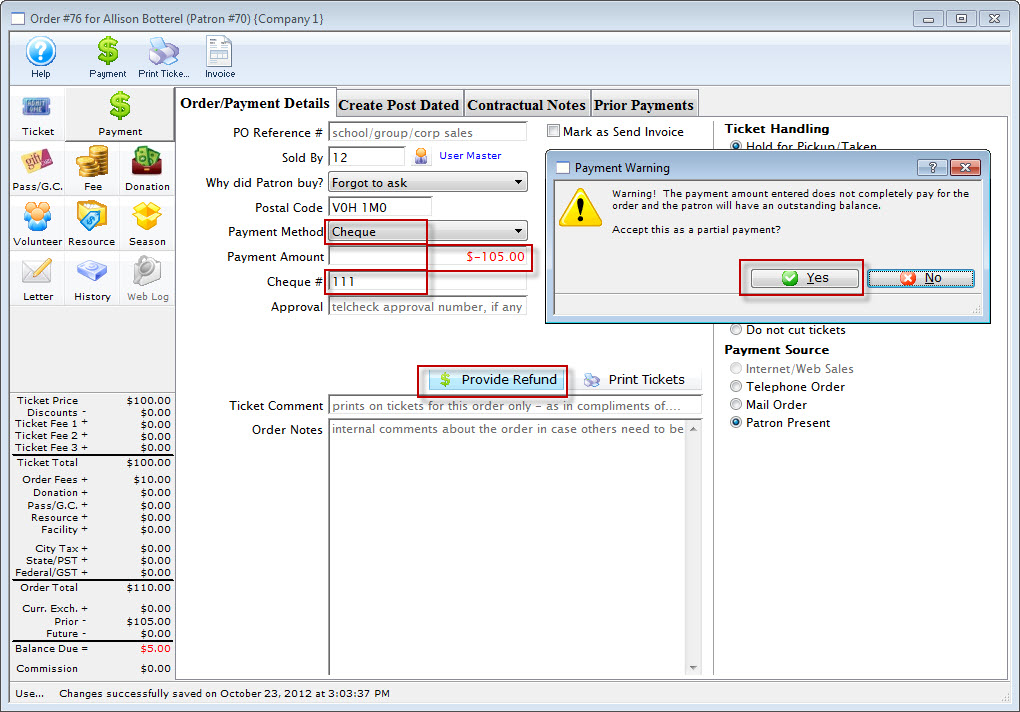

You will need to alter the payment on the Order. As the Payment has already been deposited in Theatre Manager you will not be able to delete it. Instead, you will need to reverse the payment. The steps are as follows:

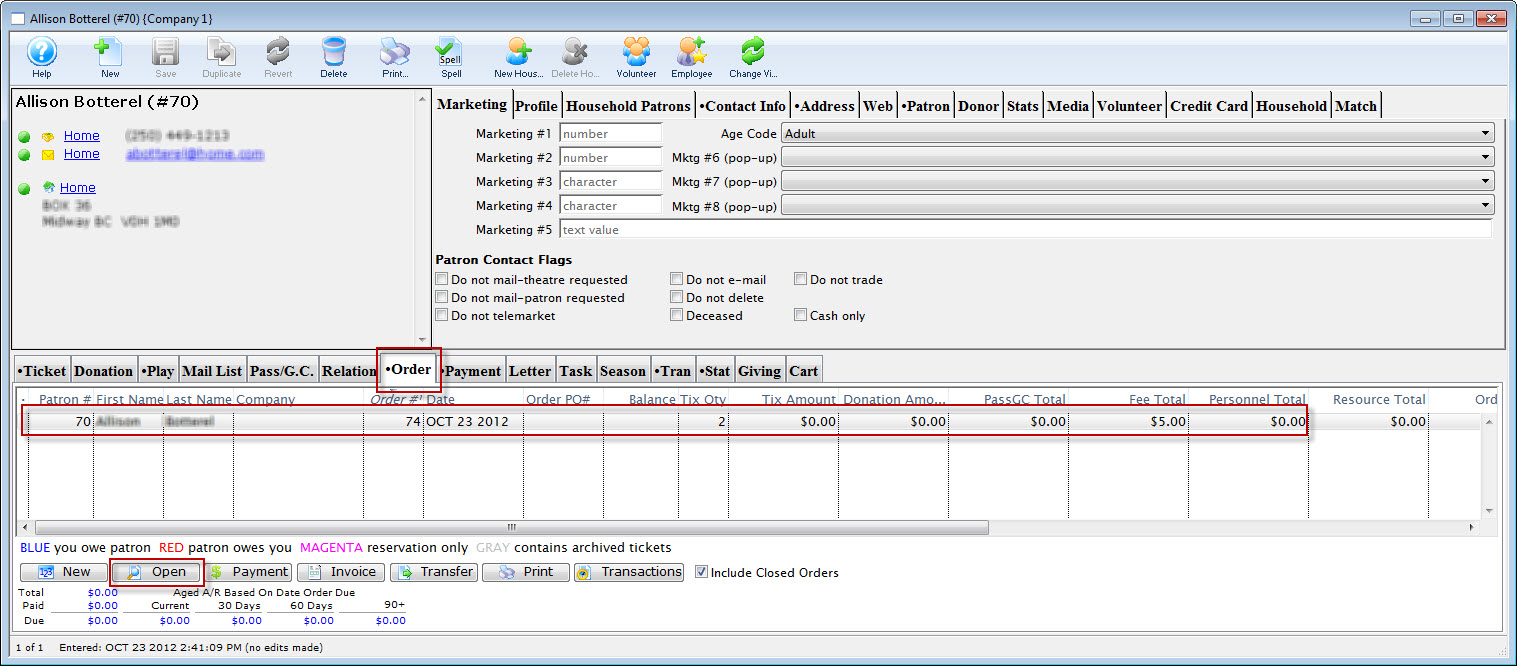

- Open the Patron Record and choose the Order tab.

- Single click on the Order the cheque payment was for and click the Open

button.

button.

- Select the fee tab and add a fee if applicable.

- Select the Payment tab.

- Choose Cheque from the Payment Method drop down, change the Payment Amount to be the amount of the NSF cheque (plus any applicable fees) and put a minus sign in front of the Payment Amount dollar value.

- Click Accept Payment.

- Click Yes to add the negative payment to the Order

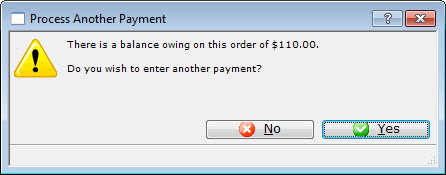

- Click No to indicate you do not wish to make another payment

The Order is now an Accounts Receivable. The patron can be contacted and arrangements made to collect the outstanding value.

Why Do My Credit Card Payments Not Appear In My Deposit?

Did Someone Else Complete A Deposit Recently?

Some organizations run the Deposit Funds step several times throughout the day. Others only complete a Deposit once and follow it with the remaining steps in the End of Day Wizard. If an Employee started the End of Day, ran the Deposit step and closed out of the End of Day Wizard, they may have deposited the Credit Cards without completing the End of Day. The Credit Card payments would not appear in the Deposit step the next time it is opened as they have already been deposited. The payments will still be a part of this Journal Entry when you Post to the GL but since they have already been sent to the bank they will not appear a second time.

To determine if the credit cards have already been deposited:

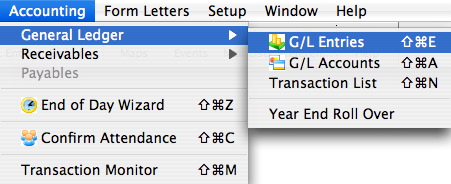

- Click the GL Entries button at the top of the window in Theatre Manager.

- Adjust the date/time range to after the last deposit was run.

- Click the magnifying glass to the far right of the date/time search option.

- Review the listed items for any deposits.

- Double click on each deposit and review the details.

When Credit Cards are deposited they will have a Deposit Reference Number and detail the date/time the deposit was completed. If you do not see a deposit for Credit Cards and you know there are cards to be deposited, it is possible something else may be causing them to not appear.

Have You Upgraded Since The Last Deposit Was Completed?

Depending on which version of Theatre Manager you were running prior to the upgrade, it is possible that changes to Employee Access may have been made that restrict some users from depositing credit cards during the Deposit step in the End of Day. To adjust Employee Access and grant access to those who are allowed to deposit credit cards, you'll need to login to Theatre Manager as a Master User.

Once login as the Master User follow the steps below:

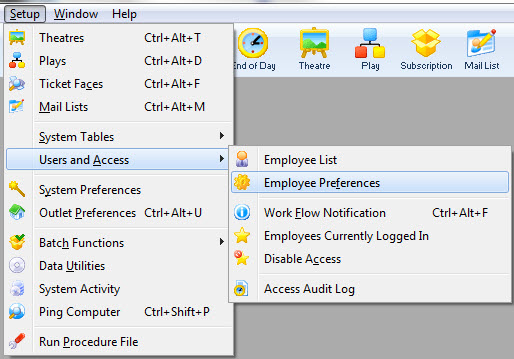

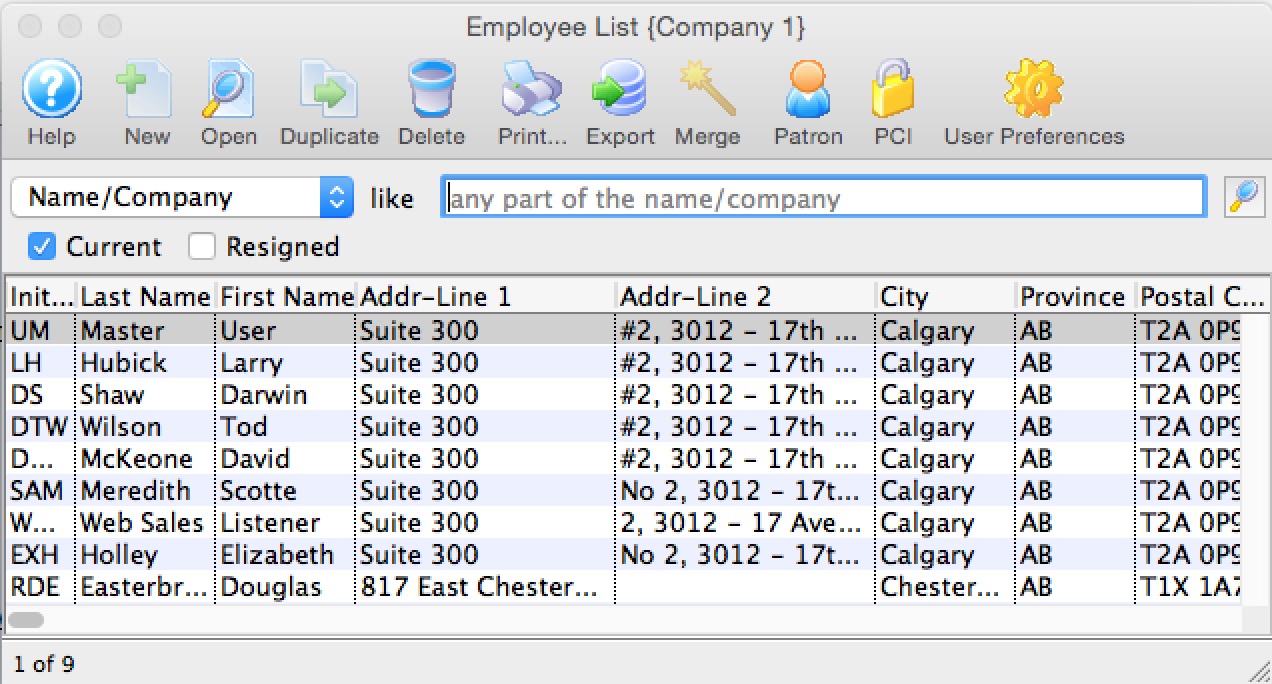

- Click Setup >> Users and Access >> Employee List.

- Search for the desired employee.

- Double click on the Employee to open their access.

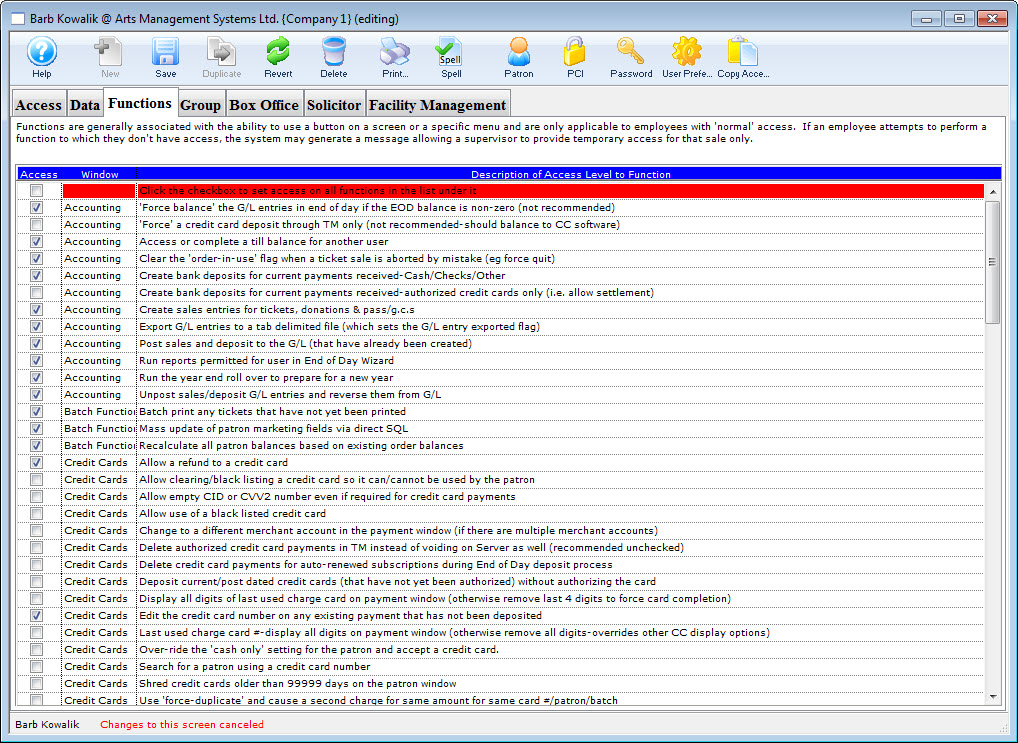

- Select the Functions tab.

- Check the box next to Accounting >> Create bank deposits for current payments received-authorized credit cards only (i.e. allow settlement).

- Close the Employee Detail window to save the changes.

In order for the change to take effect the employee will need to log out of Theatre Manager and back in.

Did You Recently Change Merchant Providers?

During the migration from one merchant account to another, the new account is setup in Theatre Manager. A part of the setup is moving employees from the one merchant profile to the other. If this step is missed it is possible the employee may be processing Credit Cards using the old merchant profile and not the new one. If this is the case you'll need to start by logging into Theatre Manager as that Employee and completing the deposit step. This needs to be done before the Employee record is updated or these cards may not be deposited. After you are sure these Credit Cards have been deposited you can update the Employee profile wih the new Merchant Account.

To edit the Employee Merchant Account setting, use the following steps:

- Click Setup >> Users and Access >> Employee Access.

- Search for the desired employee.

- Double click on the Employee to open their access.

- Select the Box Office tab at the top of the Employee Detail window.

- Click the search icon next to the Merchant # field.

- Double click on the new Merchant Account.

- Close the Employee Detail window.

In order for the change to take effect, the employee will need to log out of Theatre Manager and back in. This should be done before any additional payments are processed.

Why is there only one A/R account in TM? Can we have one for donation receivables?

- uses pure accrual accounting -and-

- inventory management (eg tickets, donations, gift certificates) does not permit separate receivable accounts in any accounting system.

- The roots of double entry accounting and the early 15th century textbook by a franciscan monk Luca Pacioli, who documented the system used by the Venetians make interesting reading.

Corner Store Example

Here is a simple example of a transaction that might occur using a corner grocery store that illustrates the difficulty in the concept:

- Your partner sends you out to buy tomatoes, lettuce, cereal and you arrive at the checkout counter. The clerk scans everything through and indicates that you owe $100.00 for your groceries. Essentially, this increases the balance owing on the order.

- Then you dig through your wallet and find you have a visa card, some cash, and coupons for $1.00 off the box of cereal. You recall that you have not paid your visa bill yet and are unsure where the remaining limit is, so you give the coupon and as much cash as you have to the cashier. Then you pay the remaining $35.00 using your visa.

- Happy with your purchases, its off home only to find out that you were supposed to pick up some romaine lettuce instead of iceberg.

- back to the store to do an exchange of lettuce, but they are out of what you need, so you settle for arugula instead (after calling home to your partner to confirm)

- This costs more, but since have no more cash left, or limit on your visa, the clerk, who knows you well says Don't worry, pay the balance next time you are in!

The simple answer is that there is just one receivable. You still owe the grocer money for the balance on the order and it is really unclear, in an inventory management system, if that balance is for any particular item. To the grocer's accountant, the plain and simple answer is that you own them money. True, you could probably allocate part of the amount owing to tomatoes, cucumbers, lettuce or cereal, but as soon as you pay part of the payment next time you are in, you will alter each of those allocations - which is a lot of work and isn't something you want to do in any accrual based system.

Thats how all accounting/inventory management systems work, bar none. I do not know of one that separates out receivables on any inventory item. Yet we know that there is sometimes a need to get a good approximation for royalty purposes or renter chargebacks.

Using Tickets and Donations Instead

You can substitute tickets, subscriptions, donations, and gift certificates for any of the vegetables above and you will find that you cannot easily separate donations receivable, given the shear volume of transactions such as:

- exchanging tickets for donations

- paying for a subscription and an annual donation at the same time using post dated visa withdrawals

- entering that annual board gift as a receivable, only to be informed by the donor that the original (large amount) was to also include 2 subscriptions and the gala dinner

How to bend the rules

We know that venues like to try to identify receivables by inventory item, specifically donations. The A/R report for order shows an allocation of donation vs other receivables using the simple rule that donations are always paid for first before any other item in an order. This report provides backup to auditors at year end, or at any time you want to see the amount that could be considered to be in donation receivables.

- Who owes you the money

- The due date & days overdue. Very important: this can be affected by setting the final payment due date in the 'contractual' tab on the payment window. If it s a school/group sale for tickets, or an ad sales where they wont need to pay for 6 months, then set the final payment date 6 months in the future. If you do that, then the receivable will say in the current column - so this can be VERY useful)

- It makes a darn good guess at whether the receivable is for donations or tickets using simple criteria (see donation balance and ticket/memb balance columns). If there is a donation in the order, then any payment pays for that first before paying for tickets or anything else.

- It tells you current/30/60/90+ days overdue.. and based on that, who to send reminder notices to.

- And, if you wish, there is the PO# column. This comes form the payment window at the top of the screen (above the reason to buy). Normally nothing is put there, but you could put 'Ad Sale' or some other tag there if you want.

You can also see an amount in the End-of-Day wizard under the A/R tab. These are accurate at the instant they are viewed.

However (heavy emphasis on this), it is not wise to put this breakdown into your accounting program. Any simple ticket exchange for a donation, or conversion of a donation from a pledge to fully paid because the patron dropped off a check, or any turning in of a gift certificate for a donation simply becomes a make-work project and violates the rule of 'make G/L entries in your accounting program from TM's G/L list - exactly as is - unchanged'.

Since Theatre Manager handles it fine for you, it is not worth tracking in your accounting system. As illustrated above, the better way is to use TM as the A/R sub-ledger and produce sub-ledger reports from Theatre Manager.

In addition, you can move all future donations into a liability account using the setup in the donation fund accounts and be able to track future donations that way.